Should I move my money when markets are falling?

If you’ve been watching the news lately, you’ll know there’s a lot going on. The conflict in Iran, oil prices climbing, markets moving up and down - it’s hard not to feel unsettled.

And when the world feels uncertain, it’s completely natural to start worrying about your own finances. Should you be doing something? Should you move your money somewhere ‘safe’? Should you be making changes?

Let’s take a breath and talk it through.

The temptation to ‘do something’

In most areas of life, taking action when things feel uncertain is a sensible response. You might fix the leaky roof before winter, or book a doctor's appointment when something doesn't feel right. You don't just sit there, you do something about it. But investing is one of the rare exceptions where that instinct can work against you.

When markets dip, it’s tempting to cash out - to lock in what you’ve got and wait for things to calm down. But selling when markets are falling usually means locking in a loss at the worst possible time. And then the question is, when do you go back in? The recovery often happens quickly and without warning, which means many people tend to miss it.

The higher long-term returns from investing exist precisely because of short-term discomfort. That’s the deal - it’s the compensation for staying put when every instinct is telling you to run.

Markets have seen this before

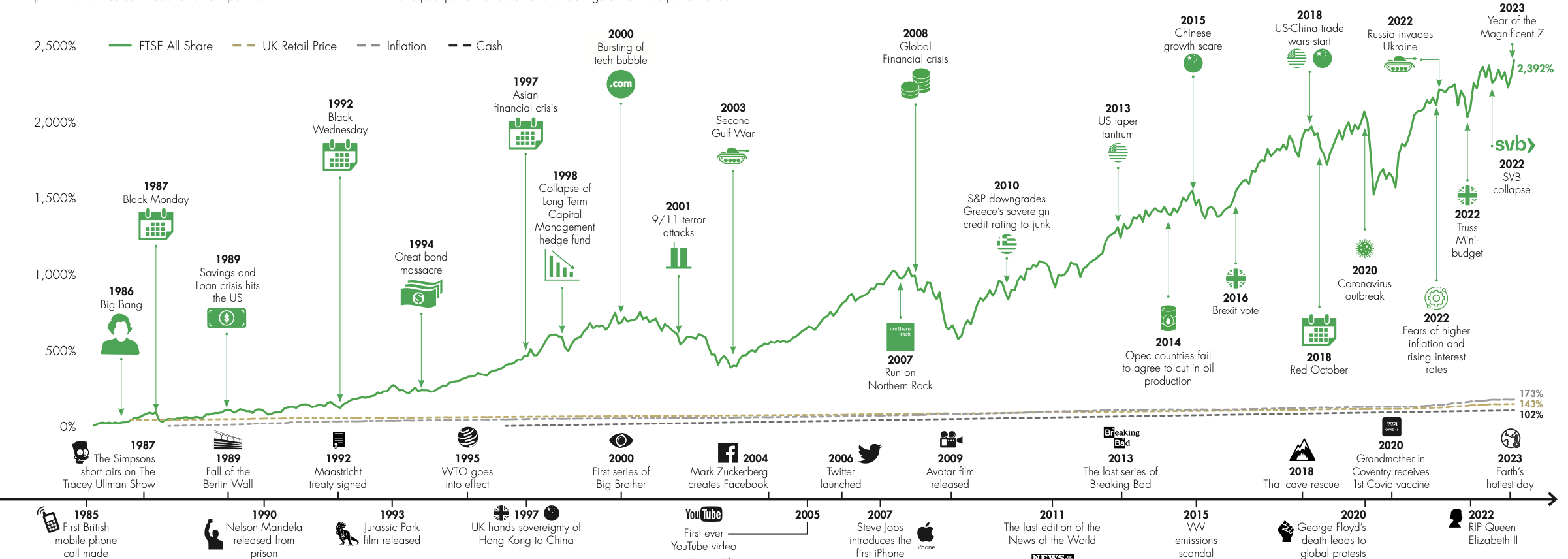

We’re not dismissing what’s happening - it’s serious, and the human cost is awful. But from a financial perspective, markets have lived through world wars, oil crises, financial meltdowns, pandemics, and countless geopolitical shocks. As you can see from the chart below from Liontrust (click to view), every time, the pattern has been the same: a sharp drop, a period of uncertainty, and then, gradually, a recovery.

That doesn’t make the journey comfortable, but the investors who come out the other side in the best shape are almost always the ones who stayed the course, rather than those who tried to time the market and got it wrong.

Your financial plan was built to handle periods like this: we plan for volatility, we diversify across regions, sectors, and asset types specifically so that no single event can knock your plan off course. That doesn’t mean we ignore what’s happening in the world - it means we don’t let it hijack your long-term strategy. This isn’t the time to tear up the plan - it’s the time when the plan earns its keep.

But what about mortgages? That’s a different story.

While the message for investments is ‘sit tight’, the mortgage market is moving fast - and here, waiting around could actually cost you.

Since the conflict began, more than 1,500 mortgage products have been pulled from the UK market. Lenders are repricing almost daily. Deals that were available in the morning are sometimes gone by the afternoon. Where you used to have days to think about a mortgage offer, you might now have hours.

If you’re coming to the end of a fixed rate, looking to remortgage, or buying a property, the window to secure a competitive deal is genuinely narrower than it has been in a long time.

We know that might feel like pressure - and we want to be upfront about that. It’s not a sales tactic! It’s the reality of a market that’s moving very quickly.

And the lenders themselves are under huge strain right now, with the sheer volume of business being pushed through at speed. That means processing times are longer, service levels are stretched, and getting things over the line takes more patience than usual on all sides.

So if you’ve been offered a deal you’re happy with, our advice is straightforward: don’t sit on it.

When to get in touch

If your circumstances haven’t changed, your investment plan probably doesn’t need to change either. But if any of the following apply, it’s worth having a conversation:

You need to make a large withdrawal in the next 6 to 18 months

Your circumstances have changed - income, health, family, work

You’re feeling anxious and just want to talk it through

You have a mortgage deal expiring or you’re looking to buy

And if none of those apply, the best thing you can do right now might simply be to carry on as normal. It might feel unnatural, but that’s usually a sign the strategy is doing exactly what it was designed to do.

We’re here if you need us. Give us a call or drop us an email - we’re always happy to chat.